In a recent post, our SAP Practice Lead, Len Riley, shared UpperEdge’s point of view on SAP’s April 10th Indirect Use announcement and some key questions existing SAP customers should consider when assessing the implications of SAP’s “Indirect Access Pricing for the Digital Age” on their organization. In this post, we will dive deeper into the key considerations for converting to the new document-based model.

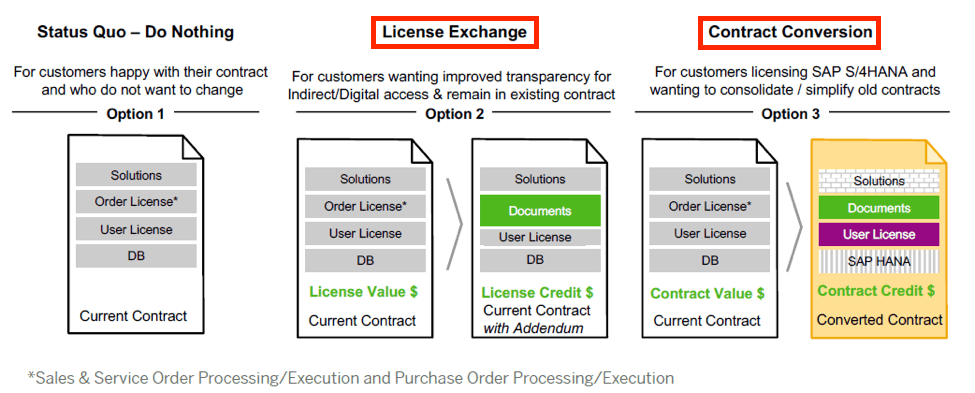

As communicated by SAP, existing customers have the option to remain under their current contract, exercise an exchange from existing user/order licenses towards SAP’s document-based licenses, or fully convert their current contract to SAP’s new licensing model.

Note that this blog focuses on Indirect Use and SAP’s new document-based model and other key areas should also be assessed when electing to fully convert to SAP’s simplified contract structure.

What is SAP Offering Under the License Exchange and Contract Conversion Scenarios?

Both scenarios lead to the adoption of SAP’s document-based model for Indirect Use, so existing SAP customers considering a license exchange or full contract conversion should understand the pricing attributes of this new model.

Key Pricing Attributes:

- There are 9 document types including:

- Sales

- Purchase

- Invoice

- Manufacturing

- Material

- Quality Management

- Service & Maintenance

- Financial

- Time Management

- Documents are weighted by level of value.

- Volume pricing structure is based on the aggregate number of documents indirectly generated in the environment.

- Credit of up to 100% of the license fees paid for the user and/or order licenses exchanged can be applied toward the new document-based model.

In addition, SAP has communicated that only the one-time creation of documents triggered via Indirect/Digital Access constitutes use and requires a license. Read-only access and any subsequent generation or modification (e.g., updates, deletions) of already created documents will not incur additional charges.

On paper, SAP’s new pricing guidelines certainly appear to be a step towards more transparency and predictability while affording existing customers the ability to preserve the value of their prior investments through equivalent credits that would mitigate the cost of moving to the new model.

Licensing Strategy Considerations for Indirect Use

Despite the favorable aspects described above, there are key questions that should be considered when assessing the appropriate licensing strategy for Indirect Use and ensuring prior investments are preserved. SAP’s new model should be assessed from a cost and predictability standpoint, but also in the context of your future IT strategy. Keep in mind that moving to the new model is irreversible, which further justifies a thorough and comprehensive evaluation of its implications.

Questions to Assess Favorability of SAP’s New Document-Based Model:

- What are SAP’s license grant/use rights for document metrics? As SAP customers know, the license grant and associated use rights reflect the true value of your investment. Although SAP has provided general metric- and scope-related information regarding its document-based model, understanding how the license grant will be contractually reflected is key to defining the scope and viability of your investment. We recommend obtaining a view of SAP’s license grant/use rights as early as possible to assess how such provision meets your company’s needs.

- How does the definition of each document type align with my current and future environments? SAP’s definition for each document type is expansive and could essentially cover a broad range of use scenarios for each business process. Ensuring you have a deep understanding of how each definition applies to the transactions generated in your environment will be critical. Your company may elect to solicit further clarification from SAP as to the scenarios that are generally in-scope and out-of-scope for each definition. This will help mitigate the risk of an unpleasant surprise after the contract is signed.

- Which model is more cost favorable from an Indirect Use standpoint? We recommend assessing the cost implications of Indirect Use under both the new document-based model and your existing contract to validate cost favorability based on your unique application landscape and projected growth. Companies that project substantial growth year-over-year will want to consider the cost impact of growing transaction volumes in their environment in the future.

- What does the future of Indirect Use look like? SAP’s new pricing guidelines for Indirect Use provide more visibility than ever and are seemingly simplified and easier to measure. However, as observed in the past, SAP’s approach to Indirect Use is progressive and ever-evolving (at least up until this point).

Driving the appropriate discussions with SAP to better understand the future is recommended ahead of any commitment. Informed customers can push for SAP’s commitment that the document-based scenarios disclosed to this day represent all potential scenarios in the scope of Indirect Access.

Questions to Ensure Any Prior Indirect Use Investments Are Preserved Under SAP’s New Model:

- Does my company have detailed visibility to its existing SAP assets and associated usage? Determining the credit that will be applied specifically in the document-based model for Indirect Use may be more challenging than it seems. Why?

1. Your company will need to understand the assets that can be exchanged towards the new document-based model, including a view of utilization within the various areas of your business.

2. The credit calculation is based on the net license fee value, which requires visibility to the net license fee paid at the license-type level.

Often, the total net license fees are identified in an aggregate manner within the Order Form with the supporting license types and associated volumes separately captured. Engaging a third party to support the process is recommended given the effort and diligence required to ensure any prior Indirect Use-related investments are appropriately accounted for under the new model.

- How will the credit value for prior investments be applied to the document-based model? SAP’s “Indirect Access Pricing for the Digital Age” material also includes a note stating that conditions will apply regarding the application of the credit towards the new document-based model. Limited information has been provided with respect to the level of flexibility that will be provided to customers as they look to reallocate their assets within SAP’s simplified licensing structure.

Before getting too deep into the solution discussions, be sure to engage early with SAP to clearly understand any limitations that could erode the value of your prior SAP investments (e.g., credits that are applicable for like-to-like business process only, any existing software not applicable for credit calculation, etc.).

Ultimately, the favorability of SAP’s new document-based pricing model for Indirect Use will likely be determined on a case-by-case basis, based on the unique aspects of your application landscape and the nature of your industry but also on SAP’s ability to address its customers’ concerns as they evaluate the implications of its new pricing model.

While now is certainly a good opportunity to dig deeper into SAP’s current and long-term strategy for Indirect Use, a majority of the preparation will need to occur internally within your organization and with your SAP representatives as you look to understand what model fits best to your IT strategy.